Why rising supply, slower sales and affordability pressures could reshape the local housing market over the next decade.

The market slows, confidence takes a knock, transactions fall away and, after a period of uncertainty, property values begin rising again. It happened after the housing downturn of the early 1990s. It happened following the Global Financial Crisis of 2008. Most Walsall homeowners, landlords and property investors assume the same thing will happen again. But what if this time is different…?

For decades, the UK housing market has followed a familiar pattern.

- Prices rise.

- Confidence grows.

- Transactions increase.

- Then eventually a correction arrives.

What if the challenge facing the housing market isn’t simply another cycle, but the beginning of a structural shift in how property values behave over the next decade?

As someone who spends every day speaking to buyers, sellers, landlords and investors across Walsall, I’m beginning to notice some interesting trends that deserve closer attention.

More Homes for Sale, Fewer Homes Selling

One of the biggest changes we have witnessed throughout 2025 and into 2026 is the growing disconnect between the number of properties being marketed and the number of properties actually completing a sale. Across many parts of Walsall, stock levels have risen significantly compared to the post-pandemic boom years.

At the same time, buyer activity has become more selective. Properties that would once have attracted multiple offers within days are now often remaining on the market for weeks or even months. This does not mean the market is crashing…far from it.

According to HM Land Registry data, average property values in Walsall remain around £218,000, with annual growth still positive. However, transaction levels tell a different story. The market is moving, but it is moving more slowly.

The Mortgage Rate Effect

For much of the period between 2009 and 2021, ultra-low interest rates fuelled extraordinary house price growth. Many buyers based their purchasing decisions not on the price of the property itself, but on the monthly mortgage payment.

When borrowing became cheap, affordability increased and buyers could stretch further. The result was simple…

- Higher borrowing capacity pushed prices upwards.

- Rising prices created homeowner equity.

- Growing equity boosted confidence.

- Confidence encouraged more borrowing.

…and the cycle repeated itself. Today that dynamic has changed.

Mortgage rates remain considerably higher than the historic lows many buyers became accustomed to. As a result, affordability has become a major challenge, particularly for first-time buyers. While wages have increased, they have not risen at the same pace as house prices over the past two decades. The consequence is a growing affordability gap that is beginning to place natural limits on future price growth.

What Does This Mean For Walsall?

The local market remains fundamentally different from many areas of London and the South East. Walsall still offers comparatively affordable housing and continues to attract buyers seeking value for money within commuting distance of Birmingham and the wider West Midlands.

However, affordability pressures are beginning to influence buyer behaviour here too. Buyers are taking longer to make decisions. Price reductions are becoming more common. Negotiation is returning to the market.

In many ways, this represents a return to a more balanced housing market rather than a collapse. The challenge arises if transaction levels continue falling while stock levels continue rising. That combination creates downward pressure on pricing.

The Stamp Duty Question

One factor often overlooked is the impact of transaction taxes. Recent changes to Stamp Duty have generated significant debate across the property industry. The intention was straightforward: increase tax revenues.

Yet early evidence suggests higher transaction costs may actually discourage market activity. When moving home becomes more expensive, fewer people move. When fewer people move, transaction numbers fall. When transaction numbers fall, tax receipts can actually decline despite higher tax rates.

Whether future governments choose to revisit Stamp Duty policy remains to be seen, but it is difficult to ignore its impact on market mobility.

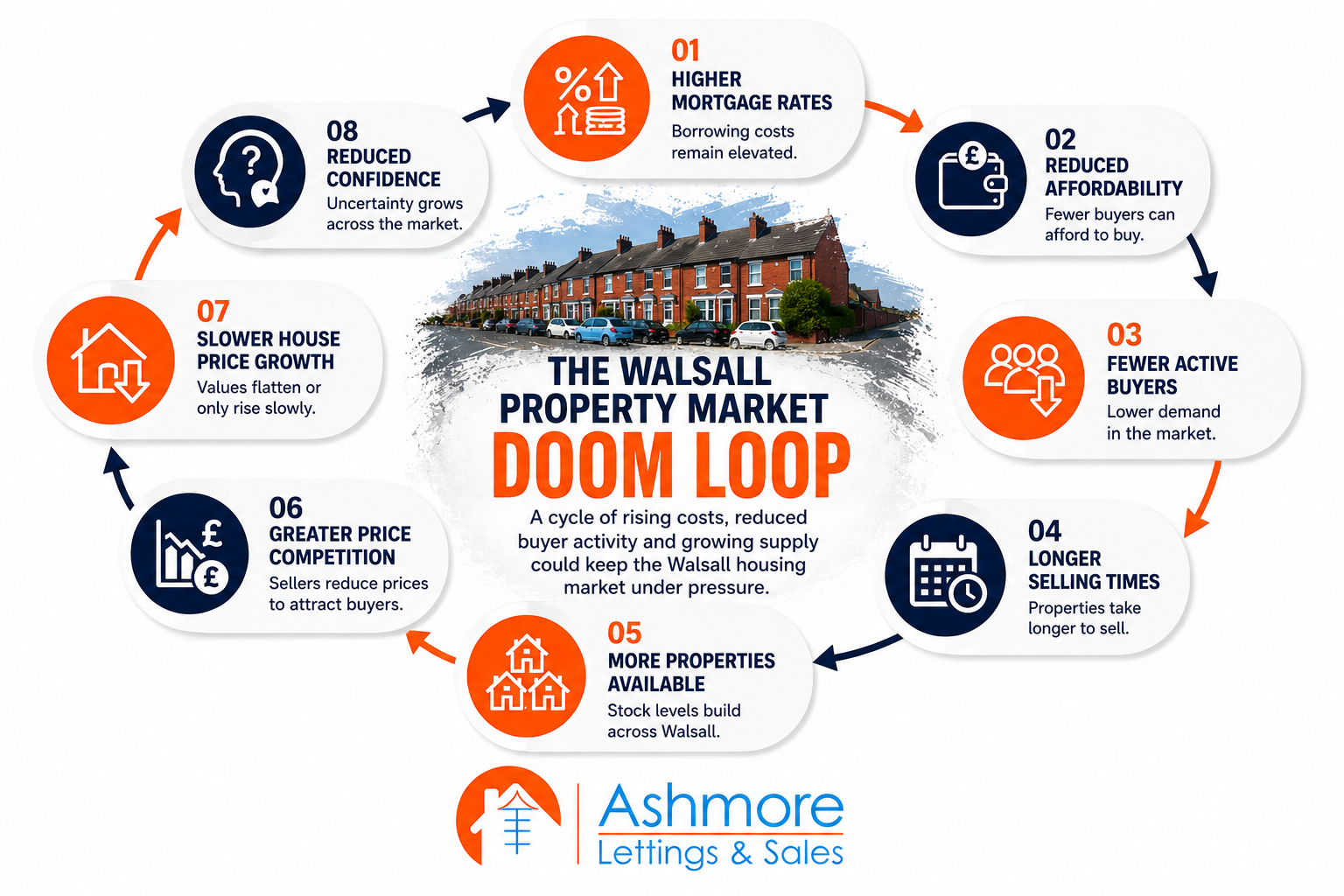

The Real Risk: Stagnation

Many people hear the phrase “property market doom loop” and immediately think of house price crashes. Personally, I think the greater risk is something else entirely…stagnation.

A market where prices barely move for years, where inflation quietly erodes real property values, transactions remain subdued and confidence struggles to recover.

Nationally, house prices have risen modestly in recent years. However, once inflation is factored in, real growth has been far less impressive. This is often overlooked because homeowners naturally focus on nominal price increases rather than inflation-adjusted returns.

Can The Market Recover?

Of course it can. Housing remains one of Britain’s most important asset classes. Population growth continues. Housebuilding remains below long-term requirements and demand for quality homes across Walsall remains healthy.

The question is not whether the market will recover but rather, what recovery looks like. The next phase may not resemble the rapid price growth experienced during the era of near-zero interest rates. Instead, we may see a period where wages gradually catch up, affordability improves and house prices grow at a more sustainable pace.

From a long-term perspective, that may actually be healthier.

Final Thoughts

The Walsall property market is not collapsing. Nor is it immune from the challenges affecting the wider UK housing market. What we are witnessing is a market attempting to adapt to a very different economic environment.

- Higher borrowing costs.

- Greater affordability pressures.

- More cautious buyers.

- Increased scrutiny of asking prices.

Whether this becomes a temporary slowdown or the beginning of a longer-term structural shift remains to be seen. What is certain is that the next few years will be some of the most important for the UK & Walsall housing market in a generation.

For homeowners, landlords and investors alike, understanding these changes early could make all the difference. I’m always happy to have a chat and hear your thoughts. Feel free to get in touch.

Don’t forget to visit the links below to view back dated deals and Walsall Property News.

Phone: 01922 637672

Email: salekm@ashmorelettings.co.uk

Wesbite: www.ashmorelettings.co.uk

Blog: www.walsallpropertyblog.com

Facebook: https://www.facebook.com/AshmoreLettings

Twitter: https://twitter.com/AshmoreLettings