As per my previous article, after receiving numerous calls and emails on the recent upcoming changes to the ‘Stamp Duty’, I feel I have to write about the subject this week…

Our Chancellor of the Exchequer, Mr George Osbourne announced in his autumn statement that from April 2016 investors buying any buy to let property will have to pay an additional 3% stamp duty in addition to the standard rate. This has caused many landlords to ask the question; whether or not purchasing a property in Walsall will still be a viable option?

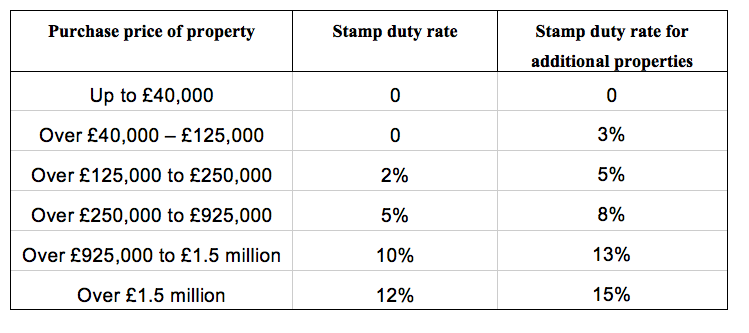

So for example, It means that the stamp duty bill for a £150,000 buy to let home will rise from the current £3,000 to £7,500 from April next year.

Many property experts are saying that property in Walsall will be worth less because potential landlords will not be willing to pay as much for them, and if house builders or existing homeowners don’t feel they are going to get as much for them, then there is less motivation to build or sell?… and the person we can blame for this is George himself. Back in 2012, he chose to utilise the British housing market to kick start the UK economy with subsidies and initiatives such as Funding for Lending and Help to Buy. However, whilst that helped the Tories get back into power in 2015, some say that this impressive growth in the UK property market has been at the expense of pricing out youngsters wanting to buy their first home.

Others say that this is the straw that is going to break the camels back as, over the next four years, landlords will slowly lose the ability to offset all their mortgage interest against tax on rental income, after changes announced in the Summer Budget. At the moment, landlords can claim tax relief on buy to let mortgage monthly interest repayments at the top level of tax they pay, typically 40%. However, over the next four years this will reduced slowly to the basic rate of tax – currently 20%.

So, that’s it then! Surely this is the end of Buy to Let in Walsall? Well, it’s not great news is it? But, before we all run to hills panicking… let me give you another thought.

Although your Stamp Duty bill will rise, George has left a significant loophole in the new rules. When it comes to selling your investment property, you can offset the purchase costs against any eventual capital gains tax; including stamp duty.

I still firmly believe that total returns from buy to let will continue to outpace other investments, such as the stock market, gilts, bonds and even pensions. Also, the best part about investing in property is that it is bricks and mortar. You can touch it, you can feel it, and it isn’t controlled by some City whiz kid in Canary Wharf… the British understand property and that goes a long way!

Buy to let has enough impetus behind it that prospective landlords will continue to buy even with a larger stamp duty bill. Walsall landlords will need to be savvy with what property they buy to ensure the extra stamp duty costs are mitigated. Buying buy to let property is a long term venture. In the past, it didn’t matter what property you bought in Walsall or at what price – you would always make money. Now with these extra taxes, the adage of ‘any old Walsall house will make money’ has gone out the window. You wouldn’t dream of investing in the stock market without at least looking in the newspapers or taking advice and opinion from others, so why would you take the same advice and opinion about buying a buy to let property in Walsall?

One source of information, opinion and advice is my Walsall Property Blog; sign up for new articles by email now!

Phone: 01922 311016

Email: salekm@ashmorelettings.co.uk

You must be logged in to post a comment.